Businesses are increasingly leveraging digital technology to reduce errors and costs, speed transactions, and drive enhanced and better customer service, according to Peter Ghavami, vice president of modeling and data science at Fannie Mae. Over the past decade, artificial intelligence (AI) and machine learning (ML) have gained traction in various industries.

Areas of AI/ML applications in the mortgage industry include automating and streamlining manual processes such as fraud detection and administrative anomalies, assessing risk management, predicting loss/default, and improving communication and personalization. This includes analysis of customer behavior.

Fannie Mae recently resurveyed lenders to assess how their views and experiences with AI/ML have changed, based on language from previous Mortgage Lender Sentiment Surveys .

Despite the growing adoption of AI/ML, we found that mortgage lenders’ familiarity with the technology, current adoption status, and implementation challenges have remained largely unchanged over the past five years. Specific findings from the 2023 survey include:

- Nearly two-thirds (65%) of lenders in 2023 say they are familiar with AI/ML technology, similar to 2018 (63%).

- In terms of implementation status, the number of financial institutions that said they had implemented AI/ML decreased significantly in 2023 (7%) compared to 2018 (14%). However, a significantly larger share said they have begun implementing AI/ML on a limited or experimental basis (22% in 2023 and 13% in 2018). Additionally, in our latest survey, fewer financial institutions (29%) say they will deploy AI/ML tools more broadly over the next two years compared to 2018 (38%).

- Among financial institutions not using AI/ML technology, the biggest barrier to adoption remained the same in 2023. These include complexity of integration with current infrastructure, lack of a track record of success, and high cost. Mortgage banks are more likely than depository institutions to cite integration complexity as a serious challenge. Data security and privacy concerns have also increased significantly since 2018.

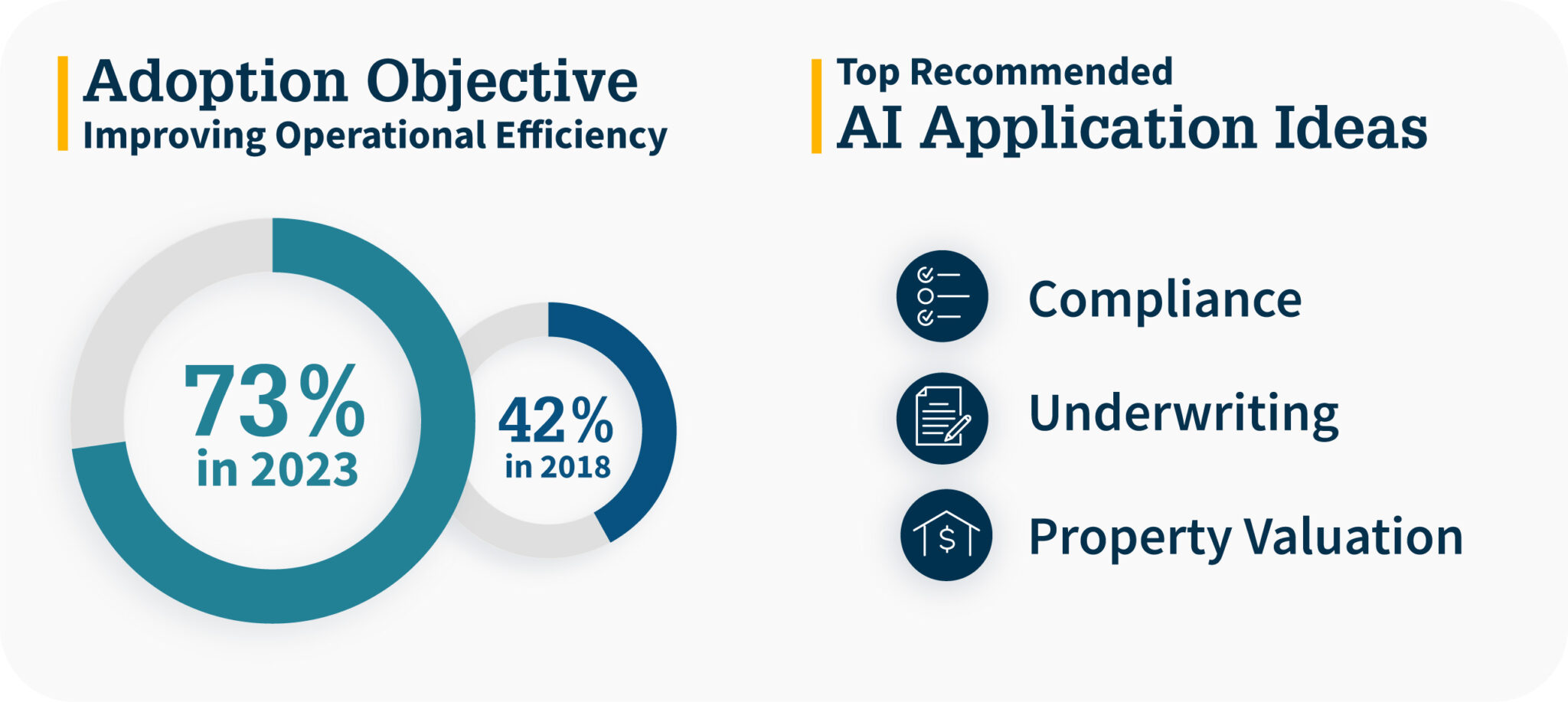

- This year, financial institutions overwhelmingly cited improved operational efficiency as the primary motivation for AI/ML adoption (73% in 2023 vs. 42% in 2018). The use case of improving the consumer/borrower experience decreased significantly (7% in 2023 vs. 41% in 2018) as the primary reason.

- For three of the seven ideas tested in the study, using AI systems to automate compliance reviews was the most appealing to lenders, particularly depository institutions. The second most appealing idea was automating anomaly detection to help identify fraud and defects early in the underwriting process. When asked to recommend ideas for AI applications that GSE would develop for the mortgage industry, the lender cited valuation automation, borrower income/employment verification, data/documentation harmonization and standardization, and compliance management. Ta.

According to Fannie Mae, these findings demonstrate a clear shift in AI priorities and provide a more grounded understanding of how AI is utilized among mortgage originators in the short and medium term. He is said to be drawing a picture. The mortgage industry consumes vast amounts of data from a variety of sources. This is a natural concern for industry players across the value chain. The latest results show that financial institutions most value AI applications that can automate this type of data processing and help identify potential anomalies. Given the rising costs in today’s business environment, AI applications aimed at improving operational efficiency are clearly well-received by financial institutions and serve as a springboard to encourage broader adoption among industry players. There is likely to be.

For years, lenders have emphasized the importance of the ‘human touch’ in the mortgage business, especially when it comes to customer interactions. Consumers similarly express a preference for human involvement in much of the home buying process, which for many is the largest financial transaction of their lives.

Either way, as these technologies mature, humans and AI/ML will play to their strengths within the mortgage industry, with the latter handling more of the back-end processing and the former building the necessary customer relationships. is expected to continue to be maintained. To increase sales.